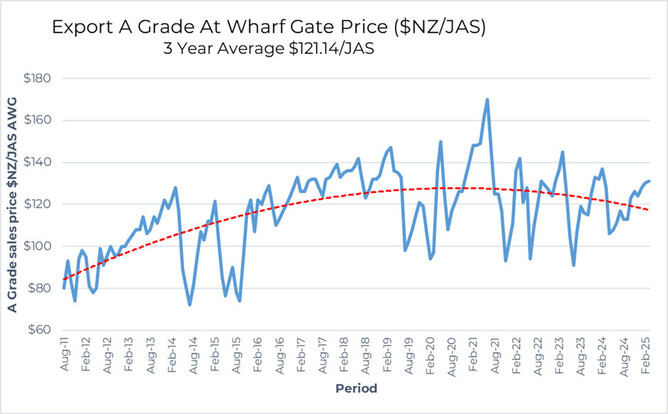

We have seen good consistent export pricing over recent months and this has continued in March with A grade prices north of the magical $130/m3 level in the North Island this has seen all crews working at 100%. Considering the uncertainty the globe is facing at present, we’re doing better than was generally expected.

The coming months are a little less certain as in the past we have seen reasonably significant falls between April and July. Hopefully this year will defy previous years. Post CNY the on-port inventory is sitting slightly over 4 million m3 and uplift has increased to between 60 and 65,000 m3 per day which is solid, FOREX is favorable at $US0.57 and shipping is in the high $US20’s to early $US30’s. There are reports of pressure on the in-market sales prices (even though some exporters pushed for increases in March) and the general consensus is a softening of some sort in coming months.

Trump tariffs continue to create much uncertainty. There’s been some retaliation from larger players and quite coincidentally, China has found quarantine pests in a load of logs from the USA subsequently suspending any imports. NZ can take that as a very small win as the USA accounts for 5% of the total softwood imports into China and every bit of competition taken out of the market helps.

A recent Reuters post stated that the China Communist Party Housing Minister, Ni Hong, announced that China’s property sector is showing positive changes, and that market confidence is improving. Hong said that “since January and February, the real estate market maintained a positive trend of stopping declines and returning to stabilization”. This, however, goes against what most analysts polled by Reuters thought and the expectation is that a recovery is not going to kick in until 2026.

India continues to be a non-event with prices very soft. Expectations that NZ can be large players in the Indian market are a bit far fetched as there are countries with ample supply that are much closer, fumigation is difficult and Indian port infrastructure is sub-par to say the least.

Back home, construction stats don’t paint a very good picture. Statistics NZ has just released data showing residential construction was down 4.9% in Q4 2024, a whopping 25% behind Q3 2022. The non-residential numbers aren’t much better with negative growth of 7.1% in Q4 2024.

It’s likely we’ll see a reversal of this trend in the first half of 2025 with lowering interest rates and boosted confidence from the departure of the Reserve Bank Governor. Interestingly, weakness in the construction sector hasn’t manifested into too many sawmill demand issues with both sawlog prices and demand relatively stable.